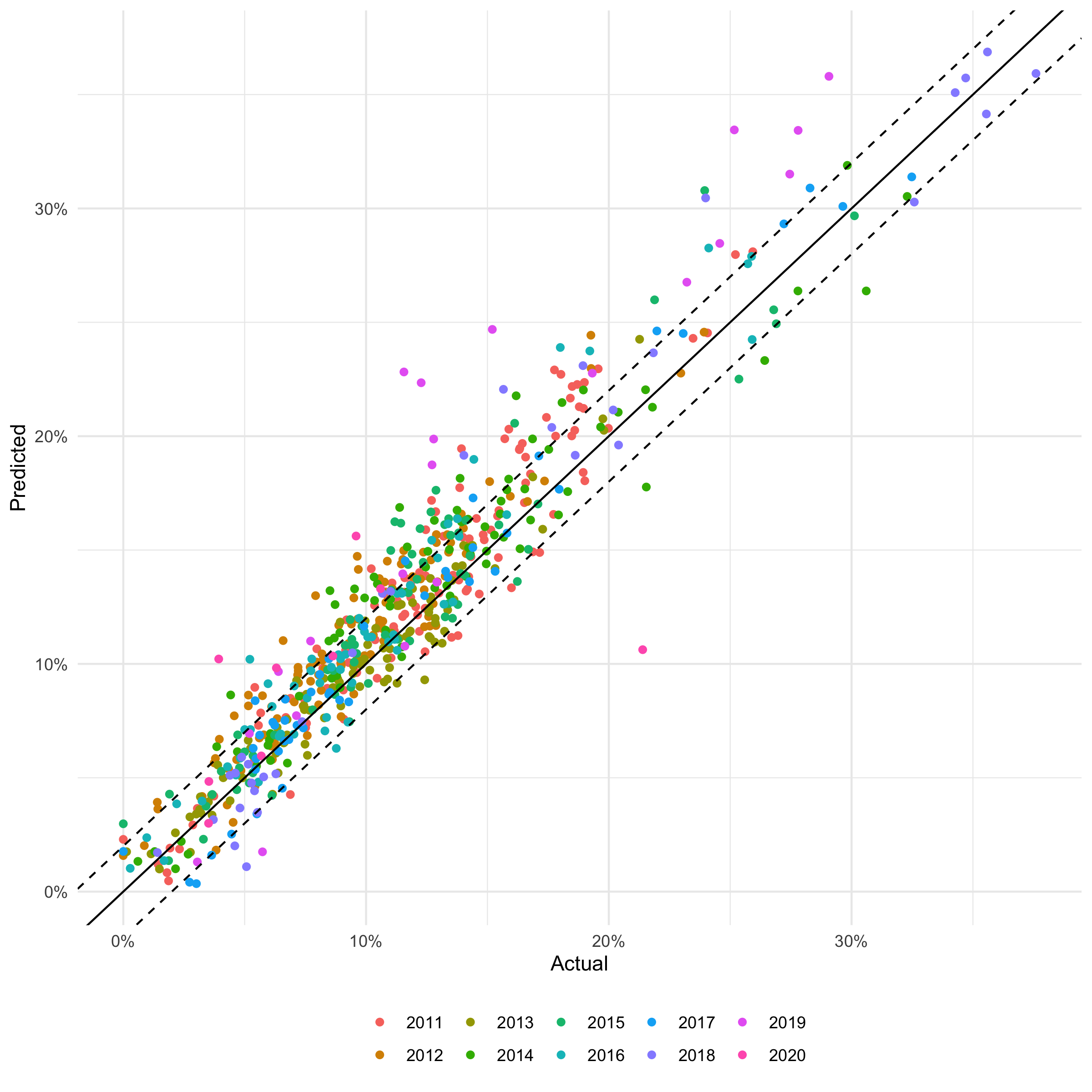

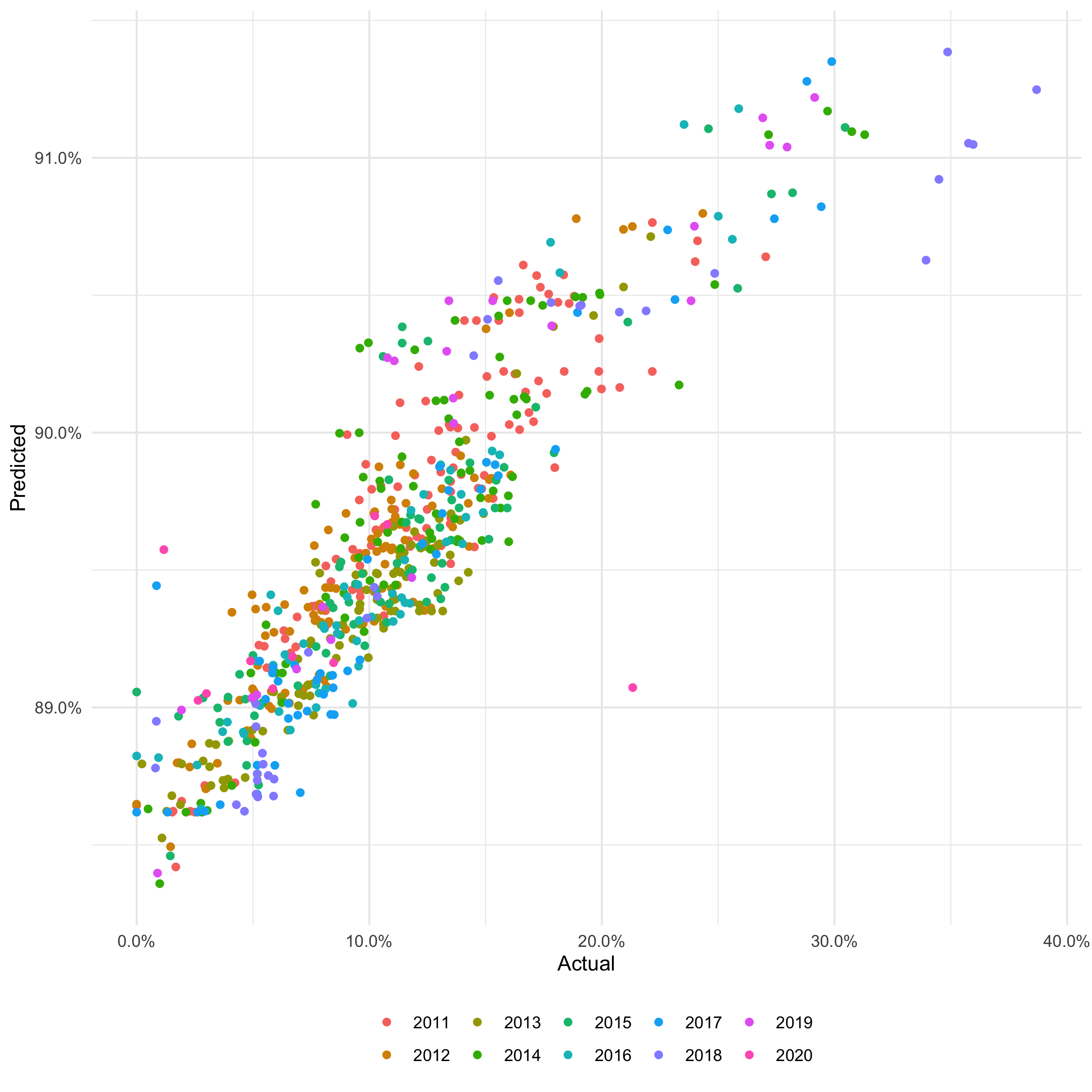

If anyone can help me understand the below behavior

- Using a lower learning rate say .01 and more trees I end up with a poorer model as measured by auc.

- Using a higher learning rate say .4 and fewer trees I end up with a superior model as measured by auc.

A smaller and more performant model is preferable to a larger less performant model. So, I am happy with the results. Still, the outcome is different that what I have learned with respect to boosting with respect to learning rate and number of trees. I suppose it is simply the difference in classifiers. Still, I would like to understand the why as best possible as I plant to replace the old classifier with XgBoost in a production environment next year.

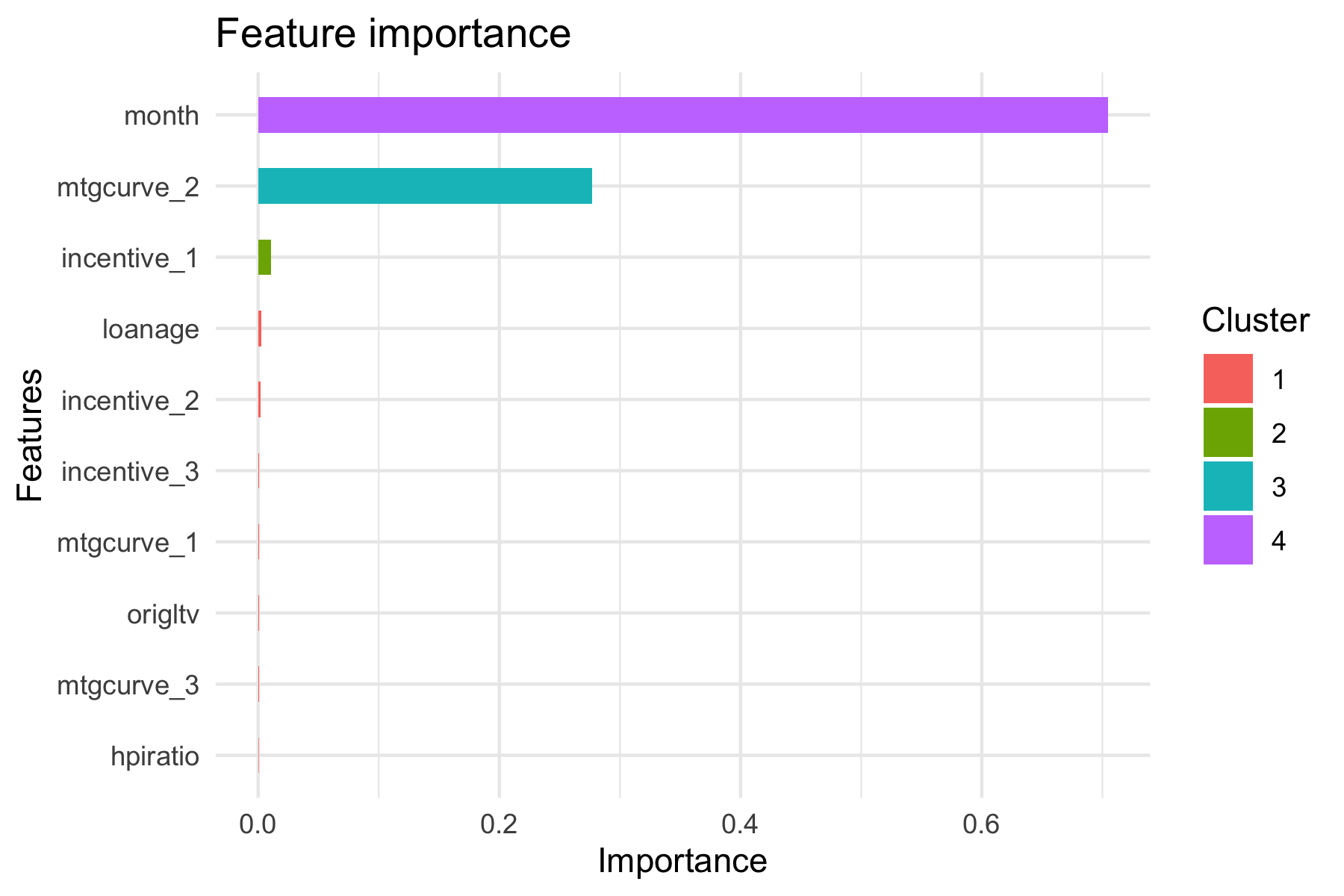

The dataset is highly unbalanced . Below is the parameter setup.

trainlabel <- trainloandata$event

trainpred <- trainloandata[,!(names(trainloandata) %in% c('event'))]

dtrain <- xgb.DMatrix(data = data.matrix(trainpred), label = trainlabel)

testlabel <- testloandata$event

testpred <- testloandata[,!(names(testloandata) %in% c('event'))]

dtest <- xgb.DMatrix(data = data.matrix(testpred), label = testlabel)

params <- list(booster = "gbtree",

objective = "binary:logistic",

tree_method = 'approx',

eta = 0.4,

gamma = 0,

max_depth = 8,

max_delta_step = 2,

min_child_weight = 1,

subsample = .5,

colsample_bytree = 1.0)

params_constrained <- params

watchlist <- list(train = dtrain, test = dtest)

xgboost_model <- xgb.train(params = params,

data = dtrain,

nrounds = 500,

watchlist = watchlist,

print_every_n = 1,

early_stopping_rounds = 5,

maximize = TRUE,

eval_metric = "auc",

metric_name = "dtrain_auc")